{kind=link}

From January to December 2022, the Vanguard Balanced ETF Portfolio (VBAL), which holds a 60/40 combine, misplaced 15.04%, practically as a lot because the 16.88% decline posted by the 100%-stocks Vanguard All-Fairness ETF Portfolio (VEQT). The issue wasn’t the shares; traders ought to anticipate volatility with them. It was the bonds.

As rates of interest spiked to fight inflation, the bond element of VBAL was hit arduous. Its higher-than-average intermediate period (a measure of fee sensitivity) meant that costs fell extra sharply than shorter-term bond holdings may need. This caught many conservative traders off guard, significantly those that believed mounted revenue would offer ballast in a downturn.

In response, many portfolio strategists started proposing a brand new mannequin: the 40/30/30. That’s 40% equities, 30% bonds, and 30% alternate options.

Whereas establishments and advisors have entry to stylish personal alternate options to make this work, the query is whether or not Canadian retail traders can replicate an analogous construction utilizing publicly listed ETFs. Right here’s my take, and a few instructed ETFs to acquire publicity to the choice house.

What’s the 40/30/30 portfolio?

The 40/30/30 portfolio is a conceptual framework that modifies the standard balanced portfolio by carving out house for various belongings. The thought is to introduce a 3rd asset class that behaves otherwise from the opposite two.

In intervals like 2022, when each shares and bonds declined collectively as a consequence of rising inflation and rates of interest, conventional diversification methods failed. The additional alternate options sleeve is designed to protect capital in instances when the opposite two pillars of a portfolio transfer in tandem.

It’s not a one-size-fits-all prescription. The 30% allotted to alternate options can fluctuate extensively relying on the portfolio supervisor’s preferences. In most institutional and advisor-led implementations, that portion might embody:

- Hedge fund-like methods similar to long-short fairness, managed futures, lengthy volatility, and market-neutral approaches that depend on quantitative fashions and multi-asset publicity to generate absolute returns.

- Arduous belongings or digital shops of worth like gold, commodities, or cryptocurrencies similar to bitcoin, usually used as static allocations to offset conventional monetary asset volatility.

- Non-public market investments similar to personal fairness, personal credit score, and direct actual property holdings, which supply long-term return potential in alternate for liquidity danger and restricted pricing transparency.

MoneySense’s ETF Screener Software

Does the 40/30/30 portfolio work?

It’s arduous to attract agency conclusions as a result of two elements restrict the usefulness of most knowledge used to help the 40/30/30 thesis.

The primary is survivorship bias. It’s straightforward to look backward and establish methods that delivered low correlation and stable returns, however that’s hindsight. Buyers didn’t essentially have entry to those funds or conviction in them when it mattered most. The hazard is cherry-picking success tales that weren’t extensively recognized or accessible on the time.

Second, outcomes are extremely time-period dependent. The efficiency of any diversified technique can fluctuate meaningfully relying on the beginning and finish dates. Just a few good or unhealthy years in alternate options can drastically skew the general return and danger profile of a portfolio.

That mentioned, there’s a comparatively sturdy benchmark with over 20 years of knowledge that helps assess the viability of the idea: the MLM Index. This benchmark tracks a scientific trend-following technique throughout 11 commodities, six currencies, and 5 international bond futures markets. It weights every class primarily based on historic volatility and equal-weights particular person contracts inside every basket. Whereas not an ideal proxy for all alternate options, it provides uncommon long-term, clear, and rule-based knowledge in an area usually missing each.

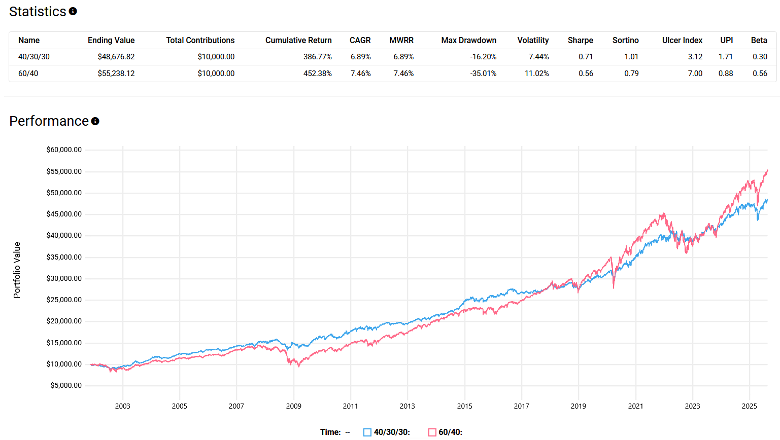

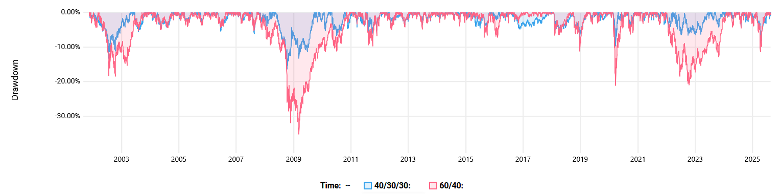

Utilizing knowledge from Nov. 12, 2001, by Aug. 19, 2025, a 40/30/30 portfolio constructed with the S&P 500, Bloomberg U.S. Combination Bond Index, and KFA MLM Index (rebalanced quarterly) underperformed a standard 60/40 combine on complete returns, with a 6.89% compound annual development fee (CAGR) versus 7.46%. Nevertheless, it considerably outperformed on a risk-adjusted foundation, with a Sharpe ratio of 0.71 versus 0.56.

Extra importantly, the diversification profit confirmed up when it mattered. The 40/30/30 portfolio demonstrated higher draw back safety throughout key stress occasions just like the bursting of the dot-com bubble, the 2008 monetary disaster, the COVID-19 crash in 2020 and the bear market of 2022.

Buyers can entry the KFA MLM Index by a U.S.-listed ETF: the KraneShares Mount Lucas Managed Futures Index Technique ETF (KMLM). It straight tracks the benchmark and supplies publicity to trend-following futures methods throughout commodities, currencies and glued revenue.

The catch? Since KMLM is U.S.-listed, Canadians face a number of hurdles: foreign money conversion, a excessive 0.90% administration expense ratio, and a 15% international withholding tax on distributions except it’s held in a registered retirement financial savings plan (RRSP).