{kind=link}

Mahindra & Mahindra Ltd – Daring by Design

Mahindra & Mahindra Ltd, the flagship entity of the Mahindra Group, primarily focuses on mobility merchandise and agricultural options. Over time, it has expanded into a wide range of service sectors, together with monetary providers, hospitality, IT, renewable power, and residential and industrial actual property. Based in 1945 and headquartered in Mumbai, the corporate is the world’s largest tractor producer by quantity. It additionally holds the highest place in India for SUV income market share, electrical three-wheeler gross sales, and three.5-ton gentle industrial automobiles. The corporate continues to be a market chief in pick-up phase for over 24 years. Mahindra operates in over 100 nations, with a world community of 47 manufacturing amenities and 21 analysis and improvement centres. Moreover, by Tech Mahindra Ltd and Mahindra & Mahindra Monetary Providers Ltd, it’s also a serious participant within the IT and finance providers business.

Merchandise and Providers

The corporate has its enterprise unfold throughout 3 essential segments:

- Auto – SUVs and LCVs, 3-wheeler, bikes and, vehicles and buses.

- Farm – Tractors and agri providers and farm equipment.

- Providers – Monetary, hospitality, logistics, renewable power, expertise, actual property, auto elements, auto recycling, pre-owned vehicles, aerospace and defence.

Subsidiaries – As of FY24, the corporate has 139 subsidiaries and 11 associates/joint ventures.

Funding Rationale

- Development methods – The corporate has not too long ago inaugurated a state-of-the-art EV manufacturing and battery meeting facility at Chakan, with plans so as to add a brand new manufacturing capability of 1,20,000 items each year on the web site. Trying forward, it additionally intends to arrange a brand new greenfield plant post-FY28 to help future progress. To strengthen its presence within the vehicles and industrial automobiles phase, the corporate has acquired roughly 59% stake in SML Isuzu. Moreover, it has entered right into a strategic partnership with Anduril Industries to co-develop and co-produce superior protection applied sciences, together with autonomous maritime techniques, AI-driven counter-unmanned aerial techniques (CUAS), and next-generation command and management (C2) software program. The corporate has additionally undertaken a number of acquisitions to broaden its renewable power portfolio.

- Launches – In FY25, the corporate unveiled its flagship electrical SUVs – the XEV 9e and BE 6e – and is establishing a devoted manufacturing facility with an annual capability of 90,000 items, supported by a capital funding of Rs.4,500 crore. Based on administration, these fashions are anticipated to redefine efficiency requirements throughout the business. Bookings are already underway, with deliveries slated for the primary half of FY26. The corporate additionally plans to introduce inner combustion (IC) engine SUVs throughout FY26. Within the Mild Business Automobile (LCV) phase, the launch of the Veero has strengthened its foothold in focused area of interest markets. Moreover, the corporate launched three new tractor fashions and broadened its three-wheeler lineup with 4 new choices.

- Q4FY25 – The corporate generated income of Rs.42,599 crore, which is a rise of 20% in comparison with Q4FY24. EBITDA grew by 20% YoY to Rs.7,911 crore. The corporate reported internet revenue of Rs.3,295 crore which is a rise of 20% in comparison with the corresponding quarter of the earlier 12 months. In the course of the quarter, the corporate has 43% market share within the Farm phase.

- FY25 – The corporate generated income of Rs.1,59,211 crore, a rise of 14% in comparison with FY24 income. Working revenue is at Rs.30,518 crore, up by 23% YoY. The corporate posted internet revenue of Rs.13,167 crore, a leap of 20% YoY. The corporate generated Rs.10,000 crore money throughout FY25.

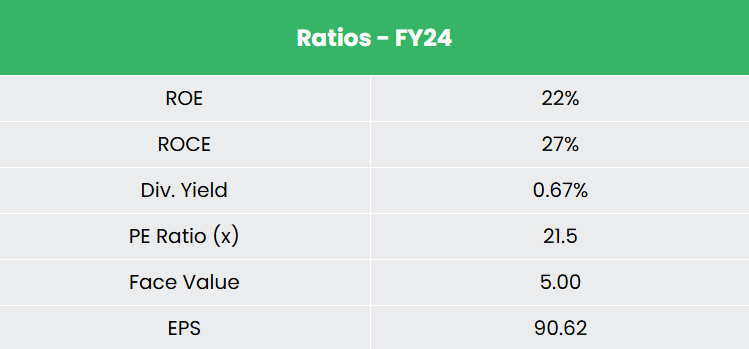

- Monetary Efficiency – The corporate has generated a income and internet revenue CAGR of 21% and 27% over the interval of three years (FY22-25). Common 3-year ROE & ROCE is round 18% and 13% for FY22-25 interval.

Business

The Indian vehicle business has lengthy served as a dependable barometer of the nation’s financial well being, given its important contribution to each total financial progress and technological progress. Presently, the sector is experiencing sturdy momentum, fuelled by substantial overseas investments, rising export volumes, and a rising concentrate on sustainability. India holds the excellence of being the world’s largest producer of tractors. In 2021, the Indian passenger automobile market was valued at US$ 32.70 billion and is projected to develop to US$ 54.84 billion by 2027, with a compound annual progress charge (CAGR) of over 9% from 2022 to 2027. The nation can be positioning itself to grow to be the world’s largest electrical automobile (EV) market by 2030, with an estimated funding potential exceeding US$ 200 billion. As a part of this transition, the Indian authorities goals for 30% of all new automobile gross sales by 2030 to be electrical.

Development Drivers

- The allowance of 100% FDI (Overseas Direct Funding) below automated route in India’s automotive sector with the sector having acquired a cumulative fairness FDI influx of about Rs. 3,22,015 crore (US$ 36.21 billion) between April 2000 – September 2024.

- Varied initiatives by the GoI similar to Manufacturing Linked Incentive (PLI), Automotive Mission Plan 2026, scrappage coverage, and many others.

- Rising demand for farm mechanization, emergence of newer applied sciences within the farming sector and continued Authorities’s concentrate on bettering the state of agriculture in India.

Peer Evaluation

Rivals: Maruti Suzuki India Ltd & Tata Motors Ltd.

The corporate is experiencing regular income progress and delivering steady returns on invested capital. Relative to its friends, it seems pretty valued and affords important potential for earnings and margin enchancment.

Outlook

New product launches have helped the corporate safe a powerful market share each domestically and internationally. Its current acquisitions are anticipated to unlock operational synergies, bolster product improvement capabilities, and broaden market attain. The corporate has earmarked Rs.16,000 crore for investments throughout FY22–27. It has additionally elevated month-to-month SUV manufacturing capability by 25%. Between 2027 and 2029, the corporate plans to supply 200,000 electrical automobiles from its Born Electrical (BE) vary. Moreover, it’s dedicated to investing Rs.1,000 crore in its Final Mile Mobility (LMM) phase.

Valuation

We consider the corporate will be capable of preserve its progress momentum, supported by a strong launch pipeline and rising operational leverage. We suggest a BUY score within the inventory with the goal value (TP) of Rs.3,747, 27x FY27E EPS.

SWOT Evaluation

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork fastidiously earlier than investing. Securities quoted listed below are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please notice that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork fastidiously earlier than investing. Registration granted by SEBI, and certification from NISM under no circumstances assure the efficiency of the middleman or present any assurance of returns to buyers.

For extra particulars, please learn the disclaimer.

Different articles you could like

Submit Views:

2,147